The year was 1998…

The global markets were rapidly devolving under a trifecta of negative events.

Russia was on the verge of defaulting on its debt. The Asian financial crisis was destroying the entire emerging market region.

And a small hedge fund based in Connecticut called Long-Term Capital Management was imploding.

It was about to derail the entire American bond market. The company had leveraged itself more than 100 to 1 and owned about a trillion dollars of American bonds.

The stock market was collapsing, and I had successfully predicted it. I was “short” the entire market. That meant that I made money as the market moved lower.

I made an absolute fortune in the early part of October… But just three weeks later, I lost everything.

Ten years of wealth creation was vaporized over a three-week period.

I was financially and emotionally crushed. That night, on the way home, I seriously thought about throwing myself in front of a train. I figured I was worth more dead than alive. It was among the lowest points of my life.

I spent the next two years analyzing what I did wrong. During this two-year journey, I studied all I could find on risk management. My trading ideas were spot-on, but I had no risk-management strategies in place to protect myself.

I traded too big, I took on too much leverage, and I didn’t know how to set and use stop-loss points. I had a lot to learn over that two-year period. So I immersed myself in the study of risk management.

By the year 2000, I returned to the financial markets. And by 2003, I had rebuilt all of the wealth I’d lost.

Losing everything actually turned out to be a blessing in disguise.

Obviously, I would never wish my experience upon anyone. However, it gave me an appreciation for risk that most investors will never apply to their personal portfolios.

And now I use two major strategies to manage risk. If you learn them, they’ll help you fully participate in blockbuster winners…

My Top Two Rules to Making Money

In my two decades on Wall Street, I’ve learned many lessons about investing. Two of the most important are stop loss risk management and asymmetric risk position sizing.

You see, you can’t get rich if you don’t know how to manage your risk first… and the first way to do that is called “Trailing Stop Loss Risk Management.”

You’ve likely heard of “stop losses” before. That’s when you set an order with your broker to sell a position when it reaches a certain price.

The trailing stop-loss price is set as a percentage below the current market price. So as the stock moves up the stop loss moves with it and is recalculated from the most recent high. (Hence the term “trailing.”)

A typical trailing stop loss is 25%… So as an example, if you bought a stock at $100, your stop loss price would be $75 ($100 minus 25%, which is $25).

And if the stock then rose to $150, your new stop loss price would be $112.50 ($150 minus 25%, which amounts to $37.50).

So should you use a trailing stop loss for every investment idea?

The answer is no.

The $2 Million Amazon “Mistake”

Say, for example, you invested $1,000 in Amazon way back when it started in May 1997. At $18 a share, you could have bought 55 shares.

What happened if you used the “typical” trailing stop of 25%?

Well, about five days later you would have sold for a 4.8% loss. Playing it safe with your tight 25% trailing stop loss means you only lost about $50…

But what if you had a bigger “risk appetite” and set your trailing stop loss at 50%?

In that case, by February 1999 – less than two years after you first bought your shares – you’d be sitting on $29,883.

Pretty darn good, right? Or is it?

Well, we all know what happened next… Amazon crashed during the dot-com bust. With the stock getting as low as $6, your decision to sell would have looked like genius-level timing. But was it?

If you had used my second type of risk management strategy, you could still be holding your shares of Amazon today. And your initial 55 shares would today be worth $2 million.

That’s a 200,766% return on your original $1,000 investment.

The Power of Position Sizing

My second risk management strategy is what I call “Asymmetric Risk Position Sizing.” In this strategy, you do NOT use a stop loss.

Instead, what you do is pick a dollar amount you are comfortable losing in a given position. I use this approach when I think there is a chance for a massive, outsized return.

The asymmetry comes from the potential gain being many times greater than the potential loss.

Typically, I suggest that you risk no more than 2.5% of your portfolio on any single investment.

So if you have a $100,000 portfolio – even if you are super bullish on any one idea – I recommend you invest no more than $2,500 in it, i.e. 2.5% of your total portfolio. And if it goes to zero… it doesn’t sink you. You can easily recover.

Does this strategy pay off?

Using our Amazon example, say you had a total $100,000 portfolio in 1997 and you decided to invest 2.5% in Amazon… Today – even if all the rest of your portfolio went to zero – your nest egg would have grown to over $5 million.

Really think about that.

That’s the power of Asymmetric Risk Position Sizing. It’s made me a millionaire many times over. And it’s changed the financial life of thousands of my readers.

Combining high-growth investment ideas with smart risk management is the surest path to life-changing profits.

Now, when do you use Asymmetric Risk Position Sizing… and when do you use trailing stop losses?

I use Asymmetric Risk Position Sizing when I am dealing with a highly volatile asset that has enormous upside but also the potential to go to zero. I use trailing stops for more traditional conservative stock investments.

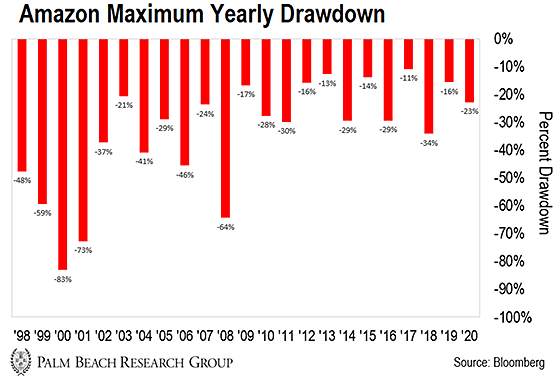

Using Amazon again, just look at how much the stock has fallen each year since it’s gone public… 48%… 59%… 73% and more. It’s enough to make your stomach churn.

We saw similar volatility in bitcoin. I first recommended bitcoin in 2016 at around $400. Today, it’s trading at $57,500 – a 14,375% gain.

Yet along the way, we saw massive drawdowns as much as 93% in bitcoin.

As you can see, my position sizing strategy would have kept you in bitcoin. And it would have prevented you from making bad decisions along the way. Just a $1,000 invested in bitcoin back in 2016 is worth as much as $143,750 today.

Again, that’s the power of Asymmetric Risk Position Sizing.

A Word of Caution

Friends, I’ll always keep you updated on which risk management strategy to use… and the optimal time to get out.

It’s the No. 1 reason I’ve been able to make my readers life-changing peak gains of 156,753%… 22,525%… and 15,806% in crypto and 3,949%, 1,738%, and 420% in the stock market.

So, please, trust the strategy. It works.

Now, just a quick word of caution: You do not want to build your entire portfolio on high-risk growth stocks or crypto investments. That isn’t a portfolio at all.

That’s why I suggest you limit your total exposure to these types of ideas to no more than 5% of your total portfolio value. (If you’re under 35, you can bump that to as high as 10% of your assets.) And again, I don’t recommend investing more than 2.5% in any single investment.

That applies to speculative blockchain plays. Or any other speculations I may recommend in the future.

As we’ve seen… you really don’t need to invest a lot of money into this strategy to change your life. In many cases, even just $200 or $400 in the right investment can be life changing.

So, remember, always be prudent. Follow my lead on when to use trailing stop losses and when to use Asymmetric Risk Position Sizing.

I believe you’ll be amazed at how much money you can make with very low amounts of risk.

Let the Game Come to You!

Teeka Tiwari

Editor, Palm Beach Daily

P.S. While we expect asymmetric investments like crypto to continue skyrocketing in the coming months, I believe this growth will spark a once-in-a-lifetime opportunity…

One that I believe will mark the biggest wealth and power shift in U.S. history.

Those who take the right steps now could set themselves up for life-changing returns and wealth… And those who don’t could get left behind.

That’s why I put together this new presentation to explain all the details…