Palm Beach Daily

Asset Location Is a Way to Minimize Taxes on Your Assets

Asset allocation is the most important concept in investing…

Numerous studies confirm it. They show asset allocation accounts for 90%-plus of investment returns.

In short, asset allocation seeks to balance risk vs. reward through portfolio diversification.

It’s done by adjusting the percentage of different asset classes (stocks, bonds, cash, etc.). Adjustments are made based on an individual’s risk tolerance, goals, and investment time horizon.

The classic “60/40 model” is a real-life example. “60/40” refers to 60% in equities and 40% in bonds. This ratio is widely used by financial advisers and institutions.

However, at Palm Beach Research Group, we use a more diversified portfolio.

It consists of eight asset classes: Equities, Fixed Income, Real Estate, Private Markets, Cryptos, Precious Metals, Collectibles, and Cash.

This broad diversification is one reason our flagship Palm Beach Letter portfolio has crushed the market for nearly a decade.

Since editor Teeka Tiwari took over in June 2016, the portfolio has posted an average annual return of 203.5%. Over the same time, the S&P 500 has an average annual return of 17.1%.

That’s correct… over the past four and half years, the PBL portfolio has beaten the stock market by an average of almost 12x per year!

You see, asset allocation is our secret sauce…

By diversifying your assets, you can generate multiple income streams from safe assets like bonds and dividend-paying stocks… and then take a portion of that safe income to speculate on “asymmetric” plays like cryptos and private equities.

These asymmetric plays allow you to swing for the fences without risking your current lifestyle.

Now, asset allocation is a strategy all serious investors must use. But there is complementary strategy many investors aren’t aware of.

And it could help you lower your taxes on all the gains you make from your asset diversification.

Think About “Where” You Invest

The strategy is called asset location. It’s the practice of locating assets in the most tax-efficient account types.

This often-overlooked strategy centers on tax minimization. With asset location, an investor can take advantage of the tax code.

You see, different types of investments and accounts receive different tax treatments.

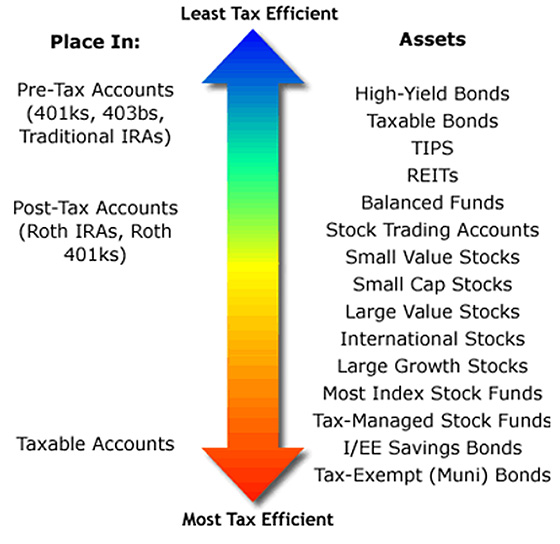

Generally, it makes sense to place less tax-efficient assets (such as bonds) in retirement accounts. And it makes sense to place more tax-efficient assets (such as stock) in taxable accounts.

If you take special care of asset placement between your taxable and retirement accounts, it can be financially rewarding.

Asset Location at Work

Here’s a simplified example of how this strategy works from financial planning educator Michael Kitces.

Let’s say an investor has $500,000 in a taxable account and $500,000 in an Individual Retirement Account (IRA), which allows you to defer taxes until you retire.

The investor plans to hold stocks in one account and bonds in the other… a 50/50 asset allocation model. The investor also plans to hold these assets for 30 years.

We’re also going to assume the bonds will return about 5% and be taxed at 25%, while the stocks will return about 10% and be taxed at 15%.

With this information in mind, here’s how each allocation scenario would play out:

Bonds held in the taxable account and stocks in the IRA

Based on the numbers above, the future after-tax value of $500,000 in bonds held for 30 years in a taxable account would be $1,508,736.

During that same 30-year period, the stocks in the IRA would grow untaxed until withdrawn by the investor. When that happens, the after-tax value of the stocks will be $6,543,526.

So, at the end of 30 years, the investor in this scenario would see a total after-tax return of $8,052,262 – a 705% gain.

Now let’s see how that compares to our second allocation scenario…

Stocks held in the taxable account and bonds in the IRA

Based on the same numbers used above, the future after-tax value of $500,000 in stocks held for 30 years in a taxable account would be $7,490,996.

During that same 30-year period, the bonds in the IRA would grow untaxed, and their after-tax withdrawal value would be $1,620,728.

At the end of 30 years, the total after-tax return on these investments would be $9,111,724 – an 811% gain.

The end result is a difference of over $1 million!

This extra after-tax wealth was accomplished by strategically allocating investments between accounts with different tax consequences.

A Simple Way to Minimize Taxes on Your Assets

If you really want to move the needle on your net worth, then you need to follow an asset allocation strategy.

As I mentioned, our asset strategy in PBL has given us returns of over 200% per year since June 2016.

But savvy investors can do even better if they add “asset location” to their asset allocation strategy. If you want to use asset location, below is a simple graphic that shows you where you should generally locate your assets.

Source: Forbes

Remember, asset allocation and asset location are not one-size-fits-all strategies. You have to know your own situation. If you’re unsure on where to place specific investments, be sure to consult your broker, adviser, or tax professional.

When making your next investment purchase, don’t just think about what to buy (asset allocation)… remember to think about where to buy it (asset location).

Regards,

Grant Wasylik

Analyst, Palm Beach Daily

P.S. Like I mentioned above, we use a diverse asset allocation model here at PBRG…

And that model includes a sector containing what Daily editor Teeka Tiwari calls the “No. 1 Investment of the Decade,” a technology poised to reshape industries like manufacturing, data storage, and security like we’ve never seen before.

If you want to set yourself up for explosive gains in 2021 and beyond, watch Teeka’s presentation right here.